European Commission - The Future of European Competitiveness

The report is a blueprint for making Europe more competitive again vis-à-vis the rest of the world and contains specific recommendations on innovation, digitalisation and advanced technologies, semiconductors and computing and AI. The report strongly criticizes the overregulation and excessive bureaucracy in the EU, arguing that they stifle innovation and drive businesses away. Draghi also emphasizes the need for reforms that make it easier to invest in European innovation and calls for a more dynamic and supportive business environment. This summary focuses on the observations and recommendations on AI in the chapters of the 400-page report.

What: Report

Impact score: 3

For who: policymakers and government officials, business and industry leaders, start-ups, academia and research institutions, venture capitalists

Mario Draghi's recent competitiveness report on the EU highlights several critical gaps in Europe’s ability to cultivate innovation and maintain its global standing. The report makes some firm observations. One of the key issues identified in the report is the low level of venture capital (VC) financing, with the EU raising just 5% of global VC funds compared to 52% in the US and 40% in China. This disparity also reflects a lower demand for VC finance. Another striking figure is that more than a quarter of the 147 unicorns founded in the EU between 2008 and 2021 have relocated abroad. Also related to tech, the EU lags behind its 2030 Digital Decade targets for fibre and 5G deployment, with an estimated investment of €200 billion required to ensure full gigabit and 5G coverage. At the same time, Europe’s industrial structure remains static, with automotive companies continuing to dominate research and innovation (R&I) spending, in contrast to the US, where investment has flowed into high-potential sectors driving productivity growth. Draghi identifies Europe’s failure to capitalize on the first digital revolution as the main reason behind the widening productivity gap with the US, but he observes that a window has opened for Europe to correct course. However, this will require tackling what he calls the most daunting challenge: the inconsistent and restrictive regulations that burden small and medium enterprises (SMEs) and stifle innovation.

The report has two parts: a strategic section and an in-depth analysis with policy recommendations. The second component consists of sectoral chapters and horizontal policies. In the horizontal policy sections, Draghi makes proposals to remove barriers to innovation and competitiveness. We highlight two proposals here:

Regulatory, legal and bureaucratic barriers

Several regulatory, fiscal, and legal differences across Member States limit the ability of EU companies to scale up efficiently and fully leverage the advantages of the EU single market. The EU’s extensive and stringent regulatory environment may, as a side effect, restrain innovation. EU companies face higher restructuring costs compared to their US peers, which places them in a position of huge disadvantage in highly innovative sectors characterised by the winner-takes-most dynamics. The EU also experiences difficulties in attracting and retaining entrepreneurial talent and skilled labour necessary to stimulate innovation.

Investments

One of the key points of the plan is the suggestion to create a better funding environment for disruptive innovation, start-ups, and scale-ups. This includes developing a European 'ARPA-type' (Advanced Research Projects Agency) agency to transform scientific knowledge into breakthrough innovation, engaging leading scientists and independent project managers to support high-risk projects. It proposes expanding incentives for angel investors and seed capital to stimulate entrepreneurial ventures and increasing the budgets of the European Investment Fund (EIF) and European Innovation Council (EIC) Fund. Furthermore, it advocates for aligning stock market regulations to facilitate IPOs, supporting venture capital through public-private partnerships, and promoting dual-use and triple-use innovation for European security and competitiveness.

Draghi also makes some observations and recommendations on a number of strategic sectors:

Computing and AI

The chapter on computing and AI is quite extensive. In the situational outline, Draghi makes some apt observations: the EU is losing its competitive edge in R&D and innovation, especially in AI, software, and computing. The EU has produced fewer leading innovators and R&D firms compared to the US and China, which dominate these fields. EU firms account for just 7% of R&D expenditure in software and internet companies, while the US holds 71% and China 15%. The EU's presence in global digital platforms is also limited, with most major platforms owned by US and Chinese companies. This trend extends to cloud computing, where US hyperscalers dominate 65% of the EU market, and EU firms capture only a 16% share. High operational costs and a lack of large-scale investment hinder EU companies' ability to compete.

Despite a strong position in high-performance computing (HPC), mostly used for scientific purposes, the EU struggles with AI adoption, with only 11% of companies integrating AI technologies compared to a target of 75% by 2030. Most foundational AI models are developed outside the EU, which creates dependency risks in key industries like automotive, banking, and healthcare. Limited venture capital, a small talent pool, and competition from US and Chinese firms further constrain EU advancements.

The EU's fragmented regulatory landscape also poses challenges, with GDPR and the AI Act creating uncertainties for innovators. The ambitions of both legislations are commendable, but their complexity and risk of overlaps and inconsistencies can undermine developments in the field of AI by EU industry actors. According to Draghi, the current frameworks may exclude European companies from early AI innovations, which creates a trade-off between strict safeguards and stimulating investment and innovation. Simplified, harmonized regulations are needed to prevent penalizing EU companies in AI development. Additionally, new EU laws like the Digital Markets Act (DMA) and Digital Services Act (DSA) aim to protect smaller players and ensure fair digital competition, but their implementation must avoid creating excessive compliance burdens.

In quantum computing, the EU has invested heavily and boasts a strong talent pool and research output. However, it lacks significant private investment. With limited technological maturity, the EU's goals, including deploying quantum supercomputers, remain distant. Overall, the EU's technological ecosystem suffers from weaker investment models, limited STEM talent, and regulatory fragmentation, which hinders its ability to scale up innovative tech companies and maintain global competitiveness. To improve, the EU must enhance financing mechanisms, attract and retain tech talent, and streamline regulations across Member States.

Objectives and proposals:

The EU must have the ambition to be a leader in developing AI for its sectors of strength, regain and retain control over data and sensitive cloud services, and develop a robust financial and talent flywheel to support innovation in computing and AI. To achieve this, the EU should aim to:

- Secure a strong position during the next five years in AI embedded in key industrial sectors, such as advanced manufacturing and industrial robotics, chemicals, telecoms and biotech based on a set of EU-developed sectoral Large Language Models and Vertical Models

- Expand the EU’s computing capability and capacity of the Euro-HPC network across Europe to serve both science and research, as well as to business ventures

- Retain control of security, data encryption and residency capabilities within EU companies and institutions and facilitate the consolidation of EU cloud providers

- Develop research excellence in quantum computing and couple EU HPC installations with quantum testing labs

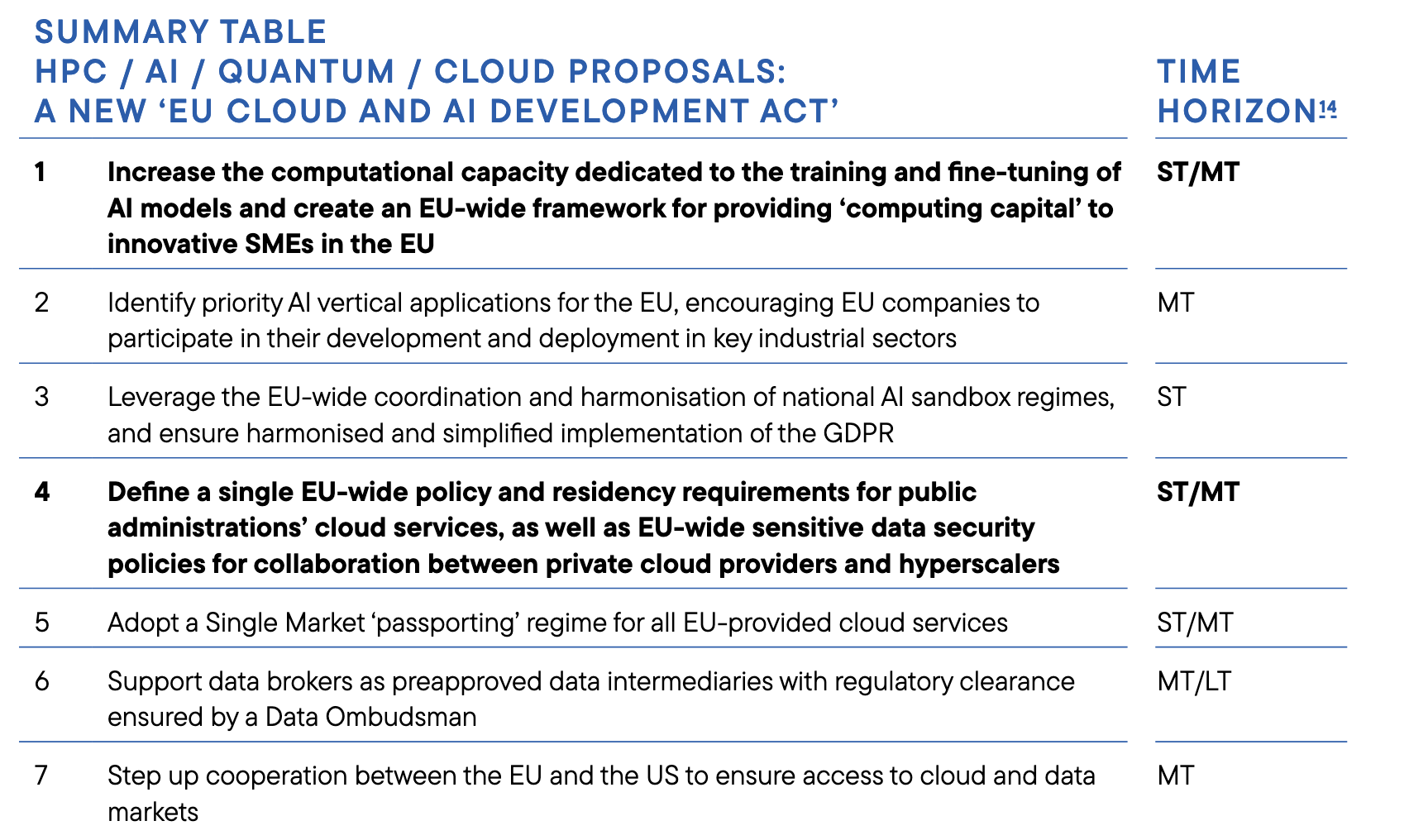

All these objectives should be bundled in a new ‘EU Cloud and AI Development Act’. That new act should strengthen European HPC, AI and quantum capabilities and infrastructure, harmonise cloud architecture requirements and procurement processes, and stimulate private involvement and investment.

Other highlights:

- To stimulate AI innovation, the EU should harmonize national AI Sandbox regimes across Member States. This should help create more experimentation in selected sectors and ensure simplified GDPR implementation. Regular assessments of regulatory hindrances should be conducted, with feedback from research centres to regulators. This should lead to periodic reviews of AI-related regulations to keep pace with technological advancements. Simplified rules, especially for SMEs, and harmonized enforcement of GDPR and AI Act provisions are essential to remove regulatory overlaps and support innovation.

- Vertical integration of AI models in strategic sectors: The EU should launch a ‘Vertical AI Priorities Plan’ to fund AI models in key industrial sectors. The report identifies ten sectors, including telecom, defence, advanced manufacturing robotics and pharma. The models should be supported by EU data sharing and should be protected from anti-trust enforcement. The plan will aim to safeguard European expertise and enhance cooperation among EU companies. Initiatives could be tendered as challenges to spur disruptive AI R&D or financed as pilot projects, with governance kept independent from businesses to ensure impartial development involving EU private and academic institutions. The vertical integration strategy should include:

- The EU should establish a dedicated ‘CERN-like AI incubator’ to coordinate key AI verticals, bringing together AI developers, Research and Technology Organisations (RTOs), and industrial players. This incubator would facilitate collaboration and replication of complex industrial environments, like factories using AI-powered digital twins. This should help combat market failure. The initiative should help EU players achieve the necessary scale in data, investment and market share to compete with US hyperscalers.

- Launch EU-level calls to finance ‘quasi-pilot lines’ within sectoral AI labs to promote EU-wide industrial research for lower technology readiness levels.

- Orchestrate ‘EU grand challenges’ to develop industrial applications, once the key problems have been framed, spinning out of the quasi-pilot lines.

Automotive

AI enables driver assistance, object detection, and lane-keeping systems. These technologies are central to developing autonomous vehicles, with a focus on fully autonomous cars expected by 2030. However, challenges remain in terms of data access, legal frameworks, and market-oriented R&D. AI can also optimize the development and production of cars and components. It can support vehicle design, and maintenance (via predictive analytics) and improve automated supply chains.

Recommendations:

- Enhance Data Sharing in the Automotive Sector: Develop incentives and frameworks to encourage data sharing among industry players to improve AI algorithms for assisted and autonomous driving. This should address current limitations in access to quality driver data.

- Harmonize Legal Frameworks for Automated Vehicles: Establish supportive legal frameworks across the EU that address data ownership, confidentiality, road access, liability, and insurance for automated vehicles. A unified approach should be developed to deploy AI-driven cars across Member States.

- Promote Market-Oriented R&D for Automotive AI: Support disruptive innovation and hardware development in the automotive sector through public-private partnerships, focusing on high-impact use cases and strengthening collaboration between public actors, Original Equipment Manufacturers and AI-driven companies.

Healthcare & pharma

The author assumes AI will revolutionise healthcare, particularly through ‘combination products’ that integrate drugs, devices, and AI algorithms to deliver personalized therapies. Despite Europe’s lower AI investment compared to North America and Asia-Pacific, AI is already enhancing diagnostics, drug discovery, and clinical trial efficiency, leading to better patient outcomes and significant cost savings. AI’s potential extends to improving the accuracy of medical diagnoses, accelerating the lifecycle of medicines, and personalizing therapies through advanced data analysis. The anticipated impact includes increased precision in treatment, expanded pharmaceutical value, and reduced healthcare costs. Also, generative AI is starting to be used to personalise therapies.

Recommendations of the report:

- Enhance Access to Quality Data: Develop a robust data infrastructure that supports internal and external data sharing, which is critical for training AI algorithms in healthcare. This requires collaboration between data scientists, business leaders, and medical professionals, alongside accelerating the digitization of health systems across the EU.

- Establish Supportive Regulatory Frameworks: Create clear and consistent regulations for AI applications, focusing on data confidentiality, safety, and model validation. Tailor guidelines to address the unique complexities of healthcare and pharmaceutical data.

- Develop a Skilled Workforce: Invest in training data scientists, AI specialists, and healthcare professionals with expertise in AI integration. Emphasize change management to ensure the successful adoption of AI technologies in healthcare settings.

- Promote Market-Oriented R&D: Encourage public-private partnerships and competitive funding for innovative AI research, particularly involving start-ups and smaller research teams. Focus on disruptive innovations and new hardware applications to expedite AI adoption in the healthcare and pharmaceutical sectors.

- Leverage the European Health Data Space (EHDS): Maximize the impact of the EHDS by facilitating access to electronic health records and scaling genome sequencing capacities, which are crucial for advancing AI-driven healthcare solutions.

- Provide clear and timely guidance on the use of AI in the lifecycle of medicines: Guidance will be gradually provided by the European Medicines Agency (EMA) and national medicine agencies until 2027, focusing on leveraging the EHDS Regulation and AI Act for analyzing clinical data and pharmacovigilance. Additionally, the secondary use of health data for research should boost R&D activities within the EU.

Energy

To fully leverage AI's potential in the EU energy sector, several recommendations should be prioritized. First, AI should be employed to enhance grid maintenance, load forecasting, and energy demand prediction, supporting the integration of renewables and enabling practices like load shifting and peak shaving. Predictive algorithms and AI-driven insights should optimize energy grid planning, asset maintenance, and building management, while AI can also improve business decisions, trading, and customer-centric energy solutions. However, challenges such as data privacy, cybersecurity, transparency, and the high energy consumption of AI itself must be addressed, with frameworks like the EU’s AI Act guiding regulation. The digitalization of energy infrastructure, access to data for training AI models, and the development of relevant skills for workers and consumers are essential. Finally, creating a collaborative ecosystem of innovators, developers, and deployers is crucial to ensure the widespread adoption of AI solutions across the energy sector.

Semiconductors

A final policy area closely aligned with AI is semiconductors. In the past Commission's reign, an EU Chips Act was presented. According to Draghi, the EU should continue this path, by strengthening its semiconductor capabilities by addressing strategic dependencies and enhancing competitiveness in key supply chain segments. It should boost R&D in mainstream and innovative product areas where it has a foothold, such as larger nodes (e.g., sensors and power controls), and develop sovereignty in design and manufacturing processes. The EU should support companies with excellence in semiconductor equipment and materials, and expand the EU Chips Act by increasing funding, accelerating innovation, and improving public-private cooperation. Key proposals should include creating an EU semiconductor budget, establishing procurement preferences for EU products, and launching a fast-track Important Project of Common European Interest (IPCEI) for semiconductor projects. Additionally, the strategy should support innovation in areas like neuromorphic and quantum computing, and provide subsidies for fabless chip design companies and foundries in strategic segments such as automotive and AI chips.

Furthermore, the EU should set up a streamlined permitting regime across Member States to facilitate the establishment of chip facilities, boost leadership in semiconductor manufacturing equipment, and manage export controls to enhance autonomy. A long-term EU Quantum Chips plan should be launched to coordinate funding and architectural decisions. The EU should also introduce a "Tech Skills Acquisition Programme" to attract and retain world-class talent in advanced electronics and semiconductors. This program should include special visas for experts, scholarships for students, and internships to link academia with industry needs. These measures would increase Europe's strategic autonomy and innovation in the semiconductor sector.